In the Input Data tab, users need to define the instruments and periods that the strategy bot will run on. The Backtester supports running the algorithm on multiple instruments and periods, providing flexibility and comprehensive analysis.

Configuration Options

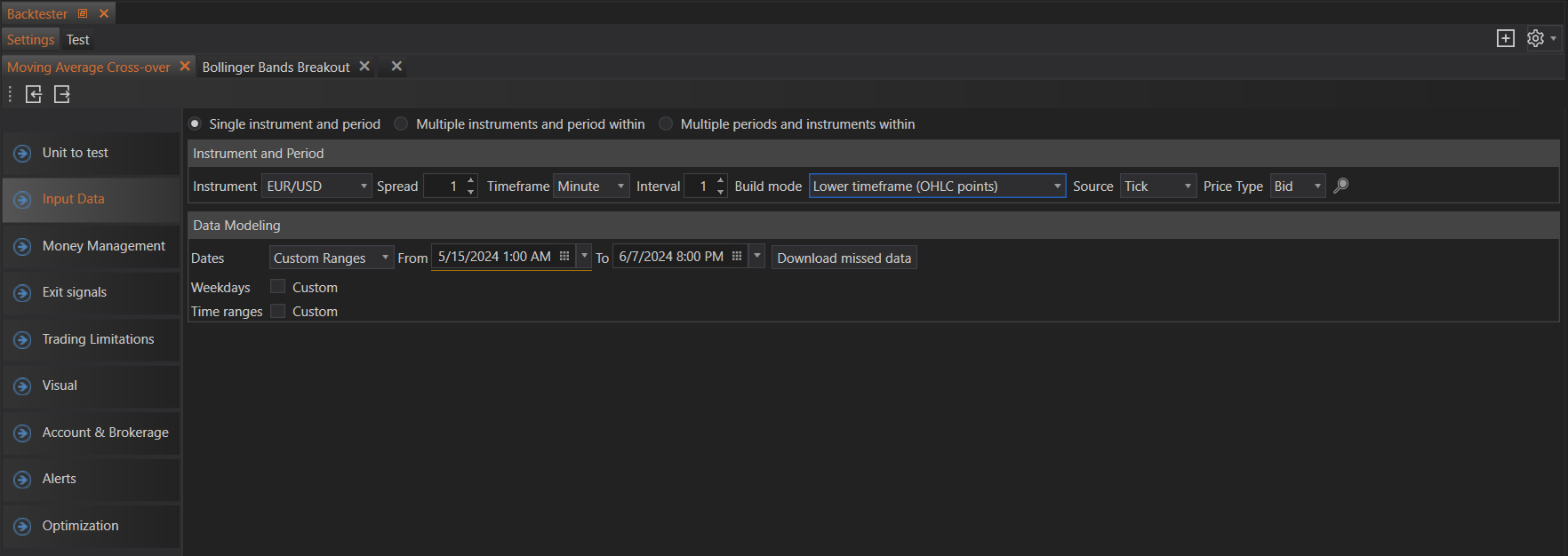

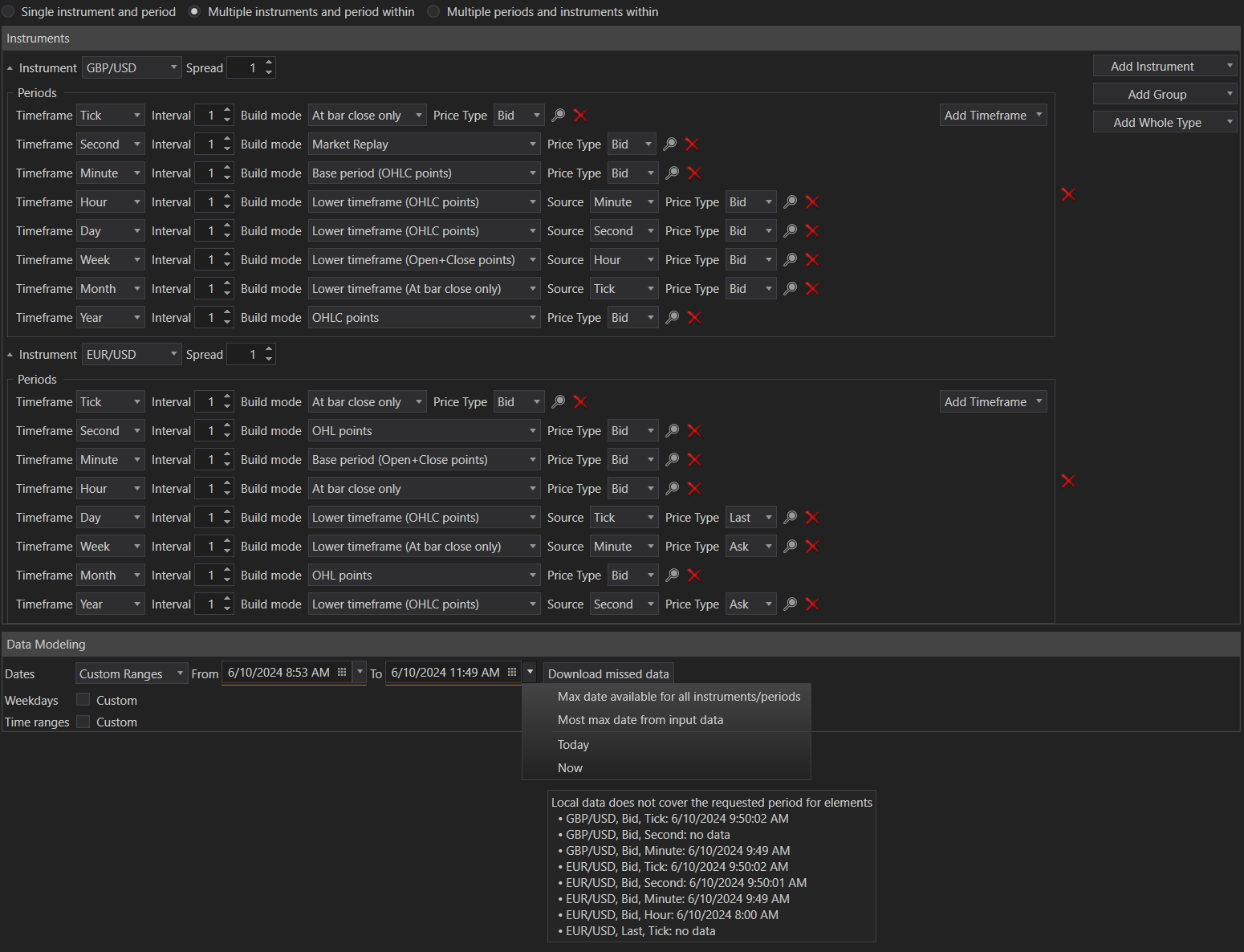

Single Instrument and Period

Description: Backtest one instrument over a single period.

Settings:

- Instrument Selection: Choose the instrument to be tested (e.g., EUR/USD, AAPL).

- Spread: Define the spread to be used during the backtest. The spread is the difference between the bid and ask price.

- Timeframe: Select the timeframe for the backtest. Options include tick, second, minute, hour, day, week, month, and year.

- Interval: Set the interval for the selected timeframe (e.g., setting an interval of 5 for minutes will test on 5-minute intervals).

- Build Mode: Select the data build mode for the backtest. This determines how the historical data is processed and used during the backtest.

- Price Type: Choose the price type for the backtest. Options include Bid, Ask, and Last price.

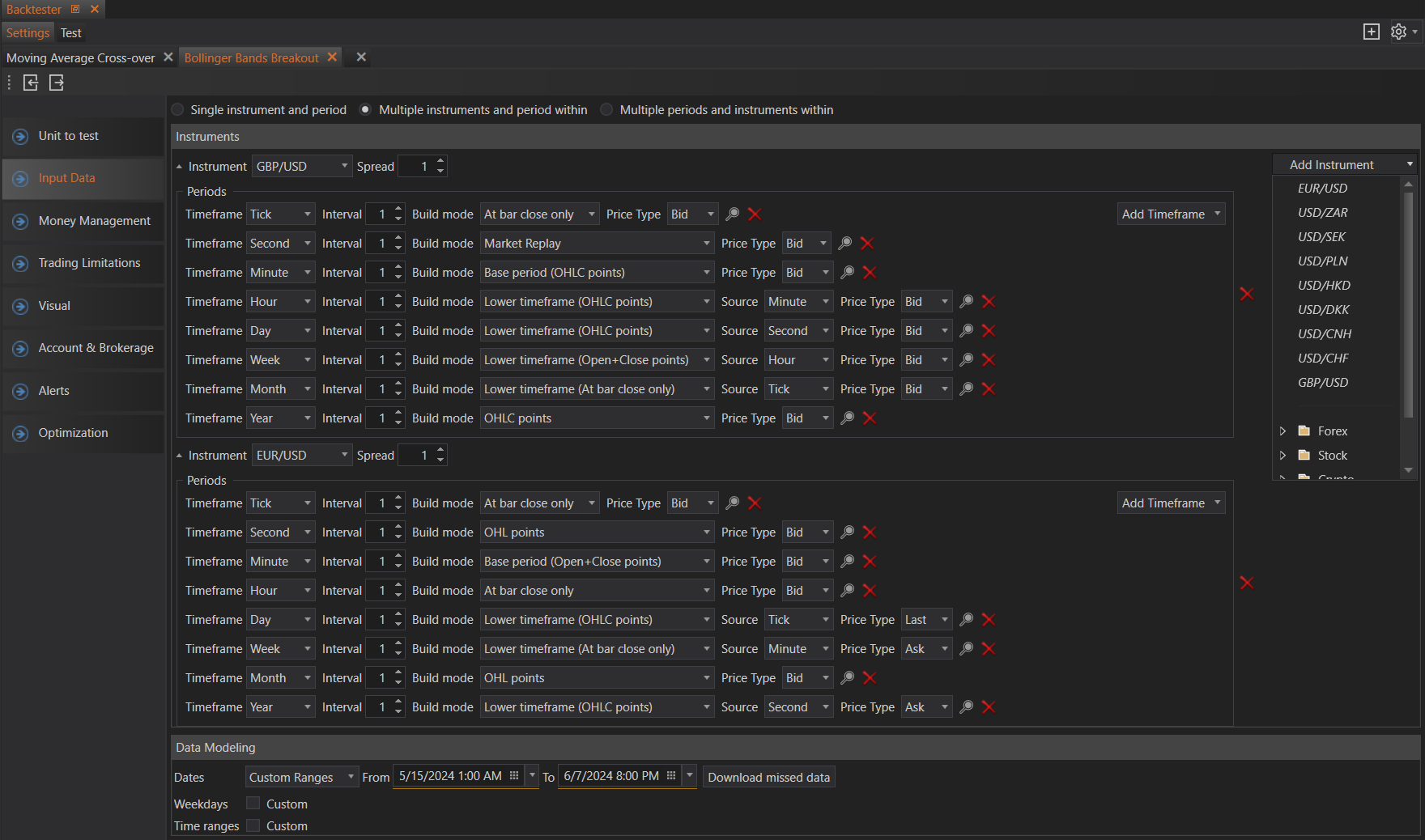

Multiple Instruments and Periods Within

This option allows users to backtest multiple instruments over multiple periods within those instruments. It enables a comprehensive analysis across different markets and timeframes, providing valuable insights into performance.

To use this option, first add an instrument, such as EURUSD. Then, set various timeframes for that instrument, such as 5 minutes, 1 hour, and 1 day, to test its performance across these intervals.

Settings for Instruments:

- Instrument: Add individual instruments one by one. This allows for precise selection of specific instruments.

- Group: Add all instruments from a specified group (e.g., all major forex pairs, all tech stocks).

- Whole Type: Add all instruments of a certain type (e.g., all CFDs, all cryptocurrencies).

Settings for Periods:

- Single Timeframe: Add a single timeframe for testing. This allows for consistent period analysis across multiple instruments.

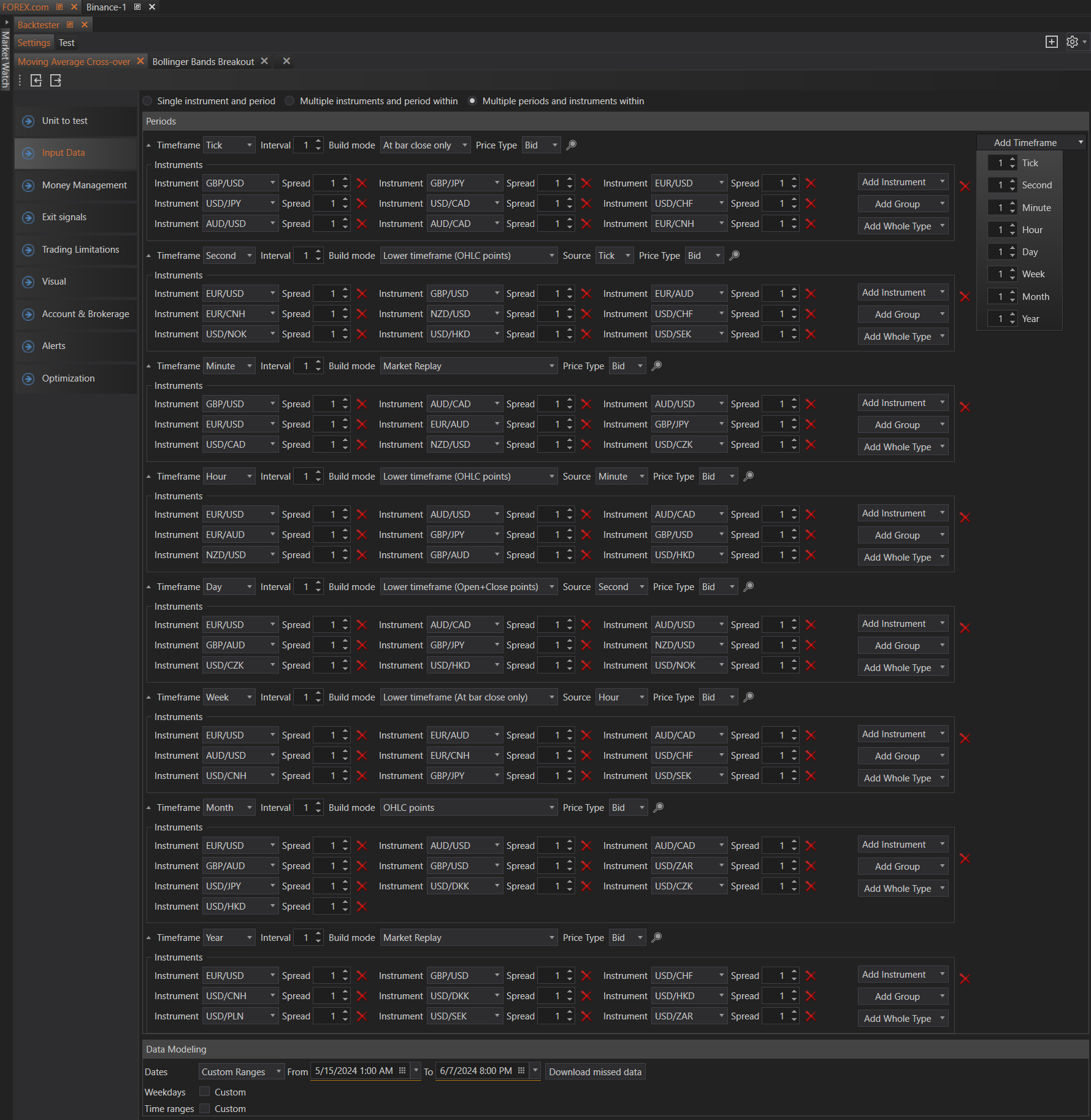

Multiple Periods and Instruments Within

This option allows users to backtest multiple periods and instruments within those periods, offering maximum flexibility and detailed analysis of how different instruments perform over various timeframes.

To use this option, first add a timeframe, such as 1 hour. Then, add all the instruments you want to test within that timeframe, such as EURUSD, GBPUSD, and others, to see how they perform on the 1-hour interval.

Settings for Periods:

- Single Timeframe: Add a single timeframe for testing. This setting ensures that each period is analyzed separately for all instruments.

Settings for Instruments:

- Instrument: Add individual instruments one by one. This detailed approach allows for precise instrument selection.

- Group: Add all instruments from a specified group, providing a broad analysis within that group.

- Whole Type: Add all instruments of a certain type, facilitating comprehensive analysis across an entire asset class.

- Market Replay: Exact tick-by-tick market replay.

- Lower Timeframe (OHLC Points): Use OHLC points from a lower timeframe.

- Lower Timeframe (Open + Close Points): Use only the open and close points from a lower timeframe.

- Lower Timeframe (At Bar Close Only): Use only the closing points from each bar in a lower timeframe.

- Base Period (OHLC Points): Use OHLC points from the base period.

- Base Period (OHL Points): Use only the open, high, and low points from the base period.

- Base Period (Open + Close Points): Use only the open and close points from the base period.

- OHLC Points: Use OHLC points for the selected timeframe.

- OHL Points: Use only the open, high, and low points for the selected timeframe.

- Open + Close Points: Use only the open and close points for the selected timeframe.

- At Bar Close Only: Use only the closing points for each bar in the selected timeframe.

Our application supports base period timeframes, including Tick, Second, Minute, Hour, Day, Week, and Month.

For example, to test a strategy on a 15-minute timeframe, you might use 1-minute data as the base period. This setup involves using 1-minute historical data to build the 15-minute intervals, ensuring a higher level of accuracy. By choosing "Lower Timeframe (OHLC Points)," the backtester can simulate detailed price movements within each 15-minute interval using the 1-minute data.

Alternatively, for testing a strategy on a 4-hour timeframe, if you set the build mode to "OHLC Points," the strategy will only be evaluated based on the OHLC points of the 4-hour data bars. This method can be somewhat inaccurate due to the limited data points. To improve accuracy, switch to "Lower Timeframe (OHLC Points)" and use 1-minute data as the lower timeframe source. This means the backtester will use 1-minute historical data to simulate the 4-hour intervals, providing more detailed and precise results. For even greater accuracy, you can select lower timeframes, such as second or tick data, which will offer an even finer granularity of price movements.

By carefully selecting the appropriate build mode and timeframes, users can ensure their backtests are both precise and relevant to their specific trading strategies. This approach allows for detailed and accurate simulations, enhancing the reliability of the backtest results.

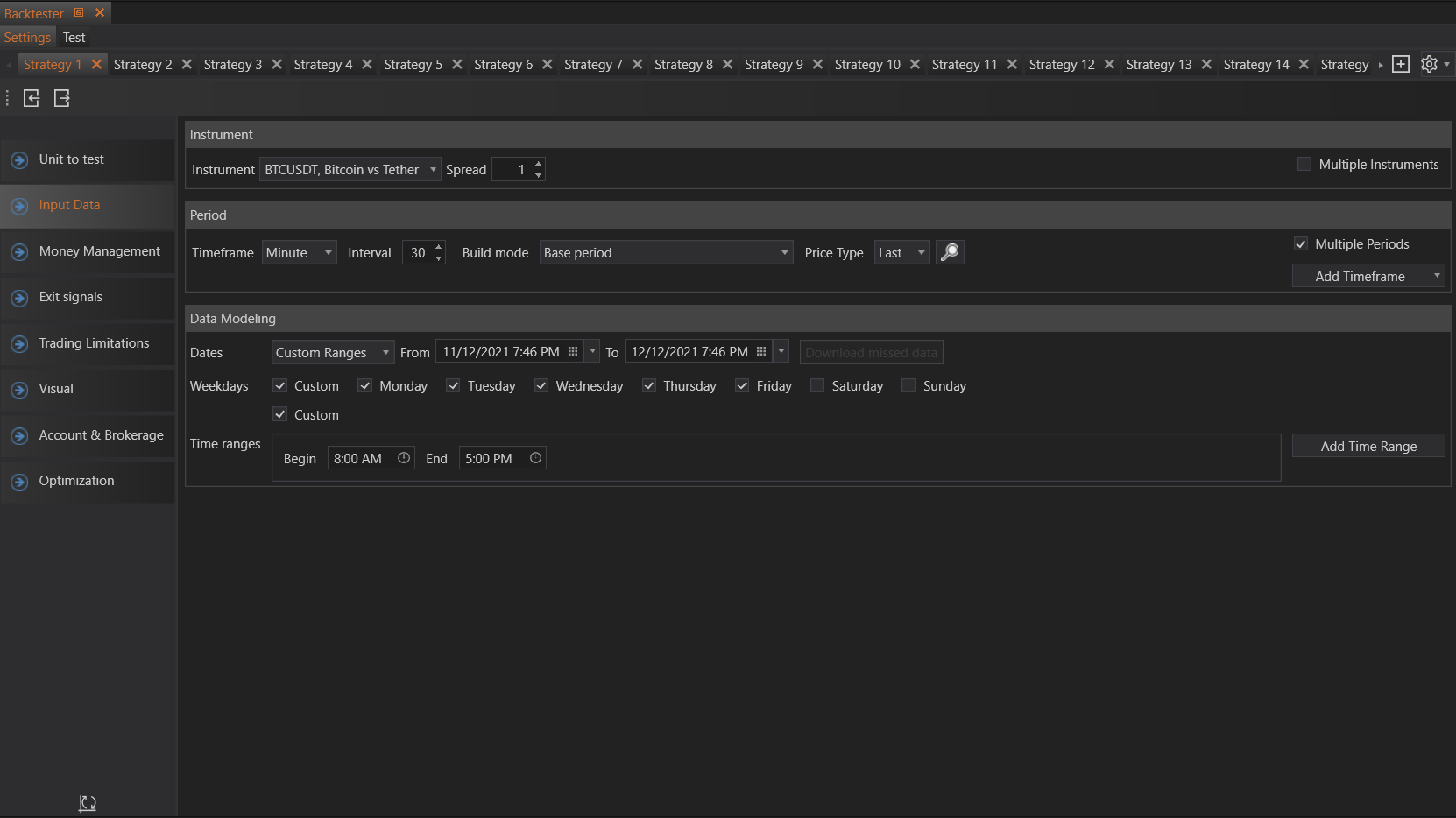

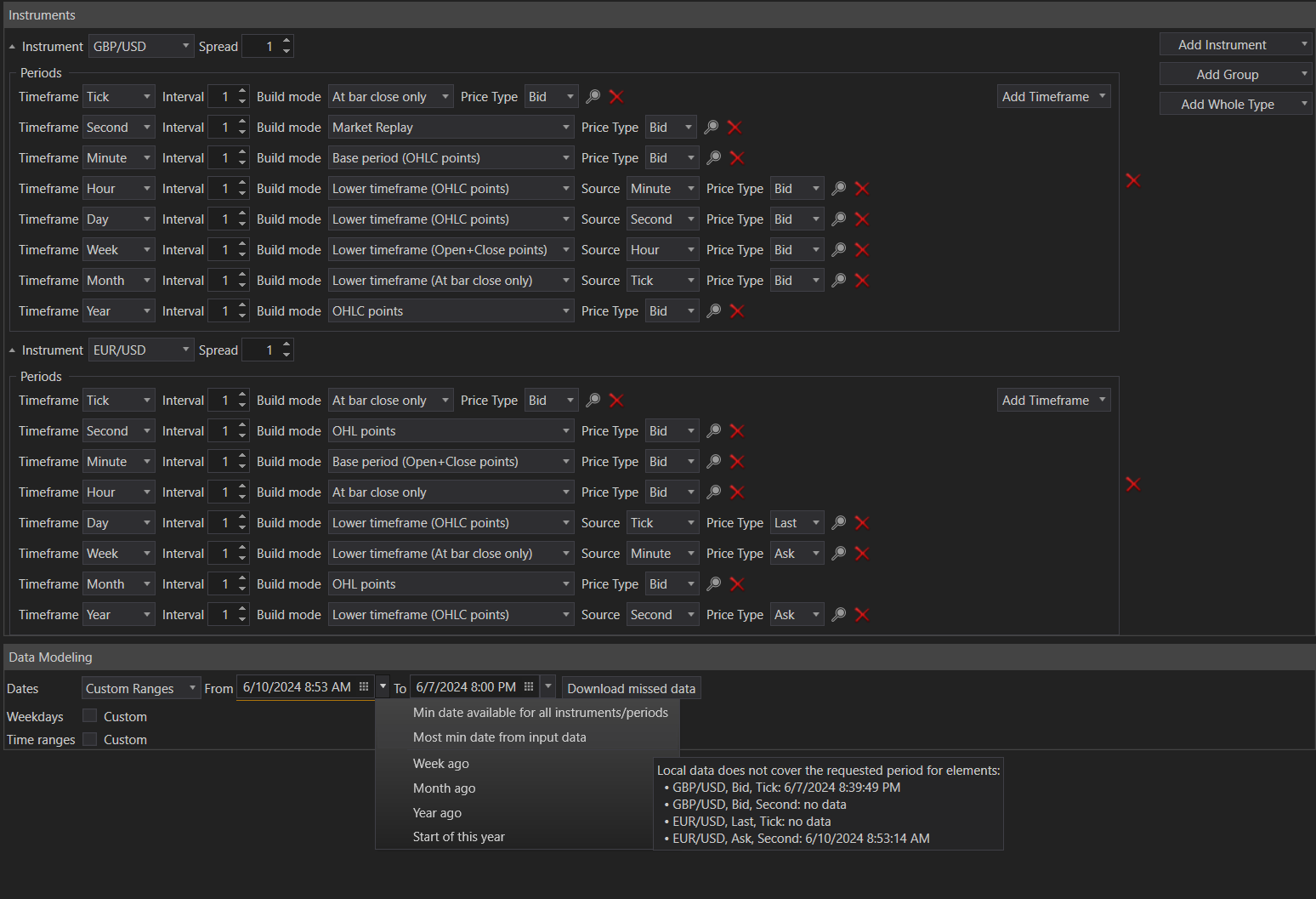

Data Modelling

The Data Modelling section allows users to define the specific parameters for how and when historical data will be used in backtesting. This ensures the backtest reflects the desired trading environment as accurately as possible.

Dates

Users can select the date range for the backtest. Several built-in date periods are available for convenience:

- Whole History: The backtest will cover the entire period for which historical data is available for the selected instruments and timeframes.

- Last Year: The backtest will use data from the past year.

- Last Month: The backtest will use data from the past month.

- Last Day: The backtest will use data from the past day.

- Start From: Users can specify a start date for the backtest, and it will run up to the current date.

- Custom Ranges: Users can define a custom start and end date for the backtest period.

When selecting Custom Ranges, users can also choose from predefined minimum and maximum periods to further refine their date selections:

-

Prebuilt Minimum Periods:

-

- Min. Date Available for All Instruments/Periods: The earliest date for which data is available across all selected instruments and periods.

- Most Min Date from Input Data: The earliest date from the provided input data.

- Week Ago: Data from the past week.

- Month Ago: Data from the past month.

- Year Ago: Data from the past year.

- Start of This Year: Data from the beginning of the current year.

- Min. Date Available for All Instruments/Periods: The earliest date for which data is available across all selected instruments and periods.

-

Prebuilt Maximum Periods:

-

- Max Date Available for All Instruments/Periods: The latest date for which data is available across all selected instruments and periods.

- Most Max Date from Input Data: The latest date from the provided input data.

- Today: Data up to the current day.

- Now: Data up to the current moment.

- Max Date Available for All Instruments/Periods: The latest date for which data is available across all selected instruments and periods.

Download Missed Data

To ensure a comprehensive backtest, all necessary historical data must be available. If data is missing, users can download it directly through the backtester interface:

Download Missed Data: Clicking this button will initiate the download of any missing data for the selected instruments and periods. Users will be prompted to confirm the action and then wait for the data to be downloaded.

Note: Data availability is dependent on the data provider. Some providers may have limitations, such as only storing up to three months of 1-minute data.

Weekdays

Users can specify which weekdays to include in the backtest. This is particularly useful for strategies that are designed to operate on specific days of the week:

- Weekdays: Select the days (Monday, Tuesday, Wednesday, Thursday, Friday, Saturday, Sunday) for which data should be included in the backtest.

Time Ranges

In addition to selecting specific days, users can also define the time ranges within each day to include in the backtest. This feature is useful for strategies that are sensitive to certain trading hours:

- Time Ranges: Specify the time ranges for each day. The backtester will only include data from these times in the backtest.

By carefully configuring these parameters, users can tailor their backtesting environment to closely match the conditions under which they intend to deploy their trading strategies. This leads to more accurate backtesting results and better-informed decision-making.