In this section

The Ranking section in the Automatic Strategy Builder (ASB) allows users to manage how strategies are generated, stored, and filtered based on specific conditions. This section provides options for defining the number of strategies to store, stopping criteria for strategy generation, filtering conditions, and selecting the type of strategy fitness metrics.

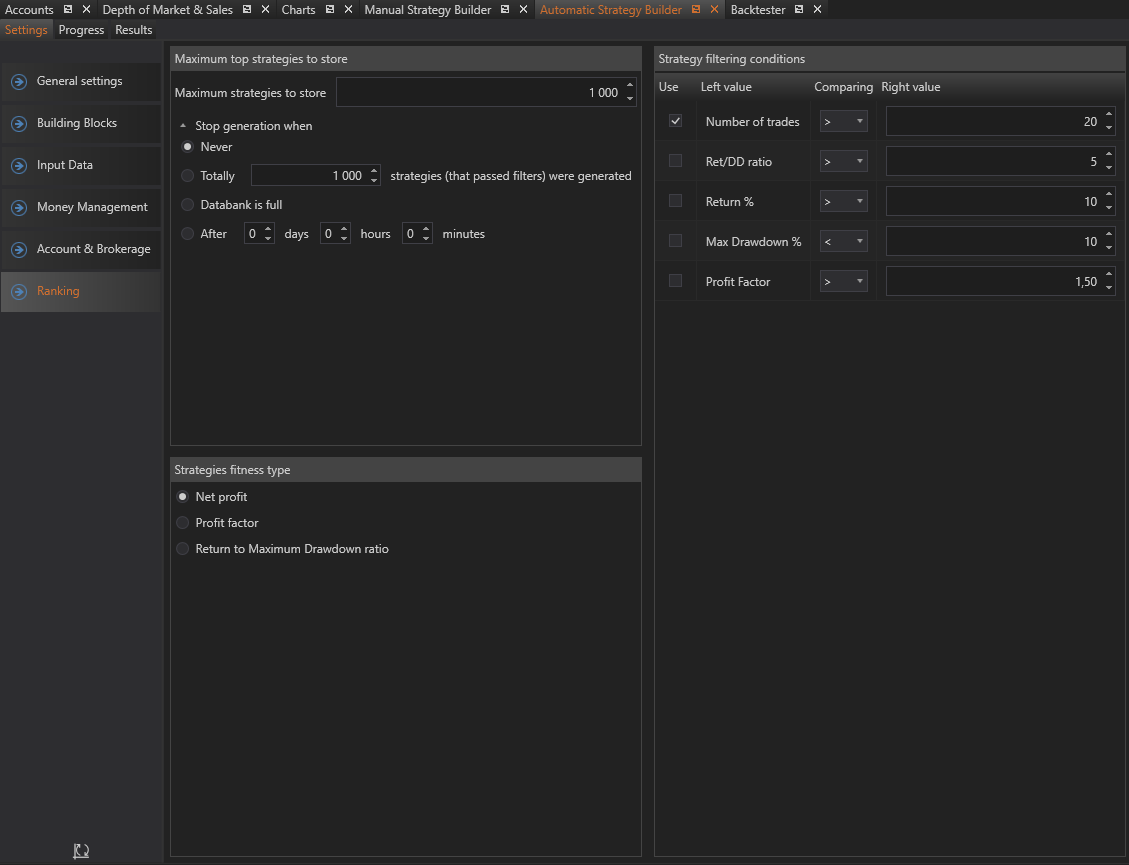

Maximum Top Strategies to Store

These settings specify the maximum number of top-performing strategies to retain. It ensures that only the best strategies, based on the user-defined criteria, are stored for further analysis and use.

Maximum Strategies to Store

This setting defines the total number of strategies to store in the databank. It limits the number of strategies kept, preventing the databank from being overloaded with too many strategies.

Stop Generation When

This setting allows users to define the criteria for stopping the strategy generation process. The available options are:

-

Never: The strategy generation process never stops and continues indefinitely.

-

Totally X strategies (that passed filters) were generated: Strategy generation stops once the specified number of strategies that meet the filtering criteria are generated.

-

Databank is full: The strategy generation process stops when the number of strategies specified in the Maximum Strategies to Store field is reached.

-

After X days X hours X minutes: Strategy generation runs for the specified duration and stops after the period entered by the user.

Strategy Filtering Conditions

Users can apply specific filtering conditions to refine the generated strategies. This ensures that only strategies meeting certain performance criteria are considered.

Use

- Check to use specific filtering condition: Enable this option to apply a specific filtering condition.

Left Value

This field allows users to specify the filter criteria. The following filters are available:

-

Number of Trades: Filters strategies based on the total number of trades executed.

-

Return/Drawdown Ratio: Filters strategies based on the ratio of return to drawdown.

-

Return %: Filters strategies based on the percentage return.

-

Max Drawdown %: Filters strategies based on the maximum drawdown percentage.

-

Profit Factor: Filters strategies based on the profit factor.

Comparing

Users can specify how the filter values should be compared:

- Higher (>)

- Smaller (<)

- Equal to (=)

Right Value

This is the input field where users enter the value to compare against the left value.

Example

Suppose a user wants to filter out strategies that have less than 20 trades. The steps would be:

- Enable Filtering Condition: Check the box to use the specific filtering condition.

- Specify Filter Criteria:

- Left Value: Select "Number of Trades."

- Comparing: Choose "Higher (>)"

- Right Value: Enter "20"

This setup ensures that only strategies producing more than 20 trades over the testing period are displayed.

Strategy Fitness Type

Users can select the type of strategy fitness metric to evaluate and rank the strategies. The available metrics are:

-

Net Profit: Evaluates strategies based on total net profit.

-

Profit Factor: Evaluates strategies based on the ratio of gross profit to gross loss.

-

Return to Maximum Drawdown Ratio: Evaluates strategies based on the ratio of return to maximum drawdown, providing a risk-adjusted measure of performance.

Summary

The Ranking section in the ASB provides comprehensive tools for managing strategy generation, storage, and filtering. By allowing users to define stopping criteria, apply specific filtering conditions, and select strategy fitness metrics, the ASB ensures that only the most relevant and high-performing strategies are retained. This flexibility and precision in strategy management enhance the overall effectiveness and adaptability of the trading strategies created within the ASB.