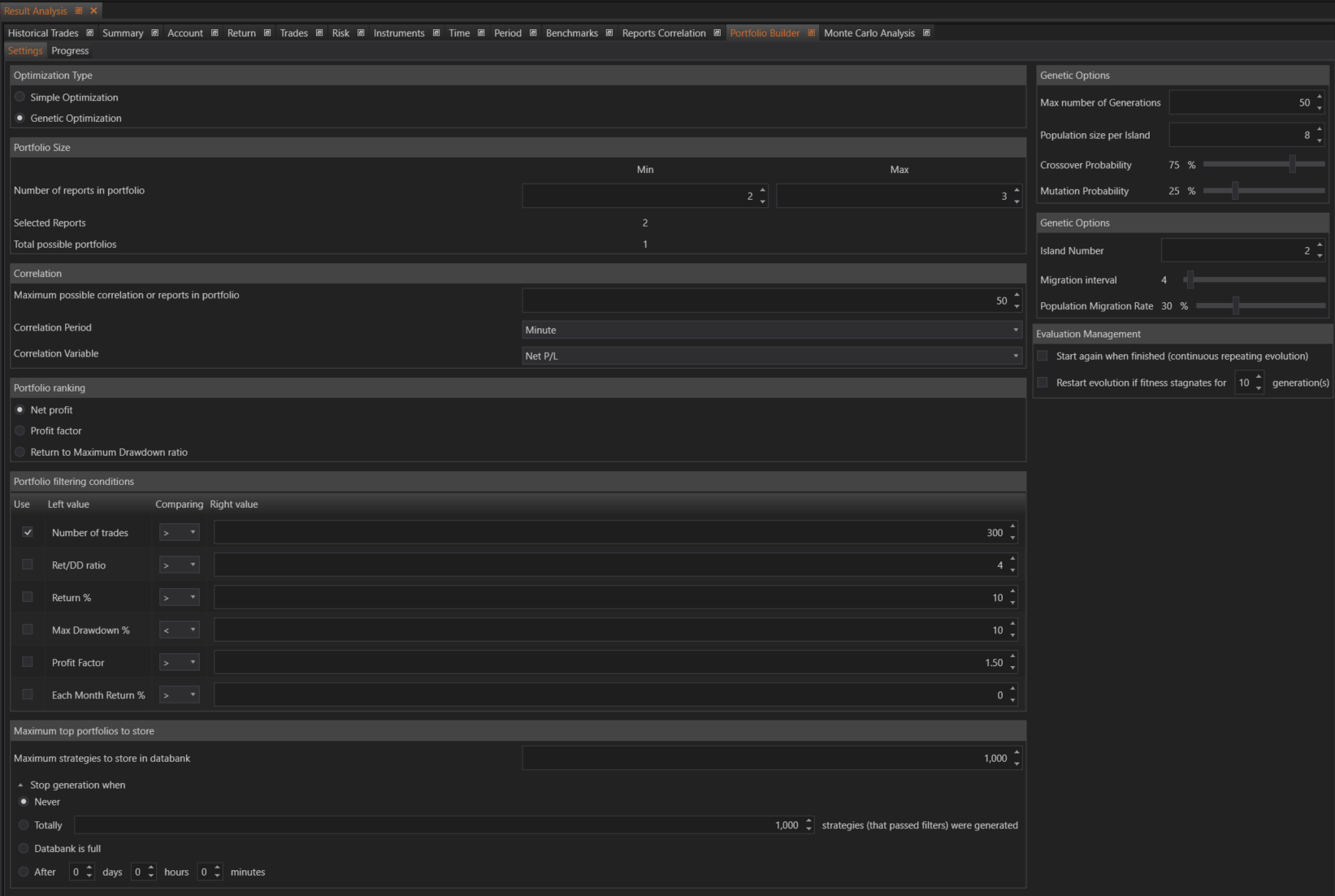

The Settings tab within the Portfolio Builder section of the Result Analysis module allows users to configure various parameters for optimizing their portfolio. These settings define how the Portfolio Builder will combine and evaluate different reports to construct the best possible portfolio based on user-defined criteria.

Optimization Type

Optimization Type allows users to choose between two optimization methods:

- Simple Optimization: A brute force approach that evaluates all possible parameter combinations. This method is thorough but can be time-consuming for large datasets.

- Genetic Optimization: Uses genetic algorithms to efficiently explore the parameter space. This method includes various settings under Genetic Options to fine-tune the optimization process.

Genetic Options (for Genetic Optimization)

When Genetic Optimization is selected, users can adjust the following settings:

- Max Number of Generations: Defines how many generations the algorithm will run before terminating.

- Population Size per Island: Number of optimizing object instances created per island.

- Crossover Probability: The likelihood that two instances will exchange genes.

- Mutation Probability: The likelihood that an instance’s genes will mutate.

- Island Number: The number of islands in the genetic architecture.

- Migration Interval: Number of generations before instances migrate between islands.

- Population Migration Rate: Percentage of the population that will migrate between islands.

Evaluation Management

This section provides options to manage the evaluation process:

- Start Again When Finished: Automatically restarts the genetic algorithm after it completes.

- Restart Evaluation if Fitness Stagnates: Restarts the evaluation if there is no improvement in fitness for a specified number of generations.

Portfolio Size

Users can specify the scope of the portfolios:

- Number of Reports in Portfolio: Defines the number of reports each portfolio should contain.

- Selected Reports: Displays the number of reports selected for the Portfolio Builder.

- Total Possible Portfolios: Indicates the total number of possible portfolios based on selected reports.

Correlation

Settings to control the relationships between reports in a portfolio:

- Maximum Possible Correlation of Reports in Portfolio: Sets a limit on the maximum correlation coefficient allowed between reports.

- Correlation Period: Defines the time period for correlation calculations (Minute, Hour, Day, Week, Month).

- Correlation Variable: Specifies the variable used for correlation calculations (Net P/L, Maximum Drawdown, Number of Opened Positions, Number of Closed Trades).

Portfolio Ranking

Allows users to rank portfolios based on specific criteria:

- Parameter: The parameter used to rank portfolios, such as Net Profit, Profit Factor, or Return to Maximum Drawdown Ratio.

Portfolio Filtering Conditions

Users can set additional restrictions to filter the strategies included in portfolios:

- Number of Trades: Limits the number of trades in the strategy.

- Ret/DD Ratio: Restricts the Return to Maximum Drawdown ratio.

- Return %: Limits the strategy return percentage.

- Max Drawdown %: Restricts the maximum drawdown percentage.

- Profit Factor: Limits the strategy profit factor.

- Each Month Return %: Restricts the monthly return generated by the strategy.

Maximum Top Portfolios to Store

Controls for storing and stopping conditions:

- Maximum Strategies to Store in Databank: Sets the limit on the number of strategies stored.

- Stop Generation When: Defines conditions for stopping the portfolio generation:

- Never: Runs indefinitely until manually stopped.

- Totally Strategies (that passed filters) Were Generated: Stops after a specified number of strategies have been created.

- Databank is Full: Stops when the databank reaches its storage limit.

- After: Stops the builder after a specified duration (days, hours, minutes).

- Never: Runs indefinitely until manually stopped.

Summary

The Settings tab in the Portfolio Builder provides comprehensive controls to tailor the portfolio optimization process. By configuring these settings, users can ensure that the Portfolio Builder operates efficiently, adheres to desired performance criteria, and produces high-quality, diversified portfolios. This flexibility allows traders to fine-tune their strategy optimization to meet specific goals and constraints, ultimately enhancing the effectiveness of their trading decisions.